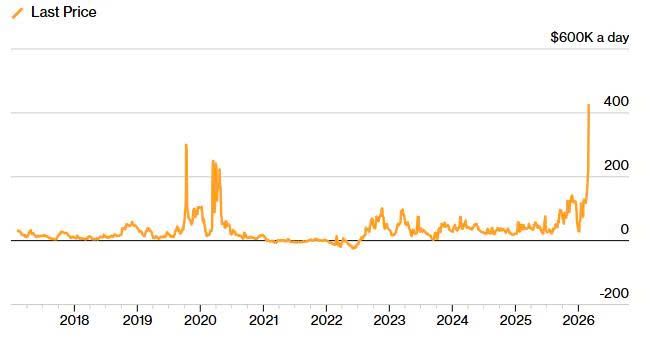

Charter rates for Very Large Crude Carriers (VLCCs) on the Middle East–China shipping route surged to approximately USD 424,000 per day after Iran effectively closed the Strait of Hormuz in early March, disrupting oil transportation and sharply increasing demand for tanker capacity.

Only three days after hostilities erupted between the United States, Israel and Iran, the supply-demand balance in the energy shipping market shifted dramatically. The impact of military tensions in the Middle East on the crude oil freight market became evident as VLCC charter rates to China soared to record levels, reflecting a significant tightening of available tonnage amid reduced vessel traffic and extended voyage distances.

Under normal conditions, VLCCs are typically chartered at daily rates in the tens of thousands of dollars. In recent weeks, however, average rates have exceeded USD 100,000 per day, and by late last week several fixtures were reported above USD 200,000 per day. On Monday, a benchmark contract for transporting crude from the Middle East to China set a new high at USD 424,000 per day, driven by robust OPEC export volumes, increased floating storage activities and constrained vessel availability.

Traffic through Hormuz is disrupted, lifting shipping costs

Source: Baltic Exchange

The surge in freight rates coincides with Iran’s announcement of the closure of the Strait of Hormuz, a vital energy transit corridor. Tanker transits through the strait declined sharply, and at certain points on Monday no crude carriers were observed moving through the waterway while dozens remained anchored on either side. Shipping activity later resumed at severely reduced levels.

In addition to heightened security risks, the withdrawal of war-risk insurance coverage by major Protection & Indemnity (P&I) clubs from 5 March has further deterred vessel deployment in the region, as many ships are unable to embark without appropriate insurance protection.

With access to the Persian Gulf constrained, refinery operators are seeking crude supplies from more distant regions, such as West Africa, the U.S. Gulf Coast, Venezuela and Brazil. Longer voyage distances have increased tonne-mile demand for VLCCs, while limited newbuild deliveries following years of low shipyard activity have contributed to short-term vessel scarcity.

Market disruptions in the Middle East have also extended to liquefied natural gas (LNG) shipping. Daily LNG charter rates climbed by roughly 40 percent on Monday, as major Qatari LNG facilities curtailed operations due to security concerns, impacting approximately 20 percent of global LNG export capacity.

Reduced LNG supply from the region has compelled major buyers in East Asia and Europe to secure cargoes from the U.S. and Australia, increasing voyage distances and tanker demand. Concurrently, European natural gas futures prices rose by approximately 50 percent amid tightening supply conditions.

From a global energy logistics perspective, the disruption at the Strait of Hormuz is reshaping crude oil and gas trade flows. Extended shipping distances coupled with limited tanker availability continue to exert upward pressure on freight rates for both oil and LNG carriers.